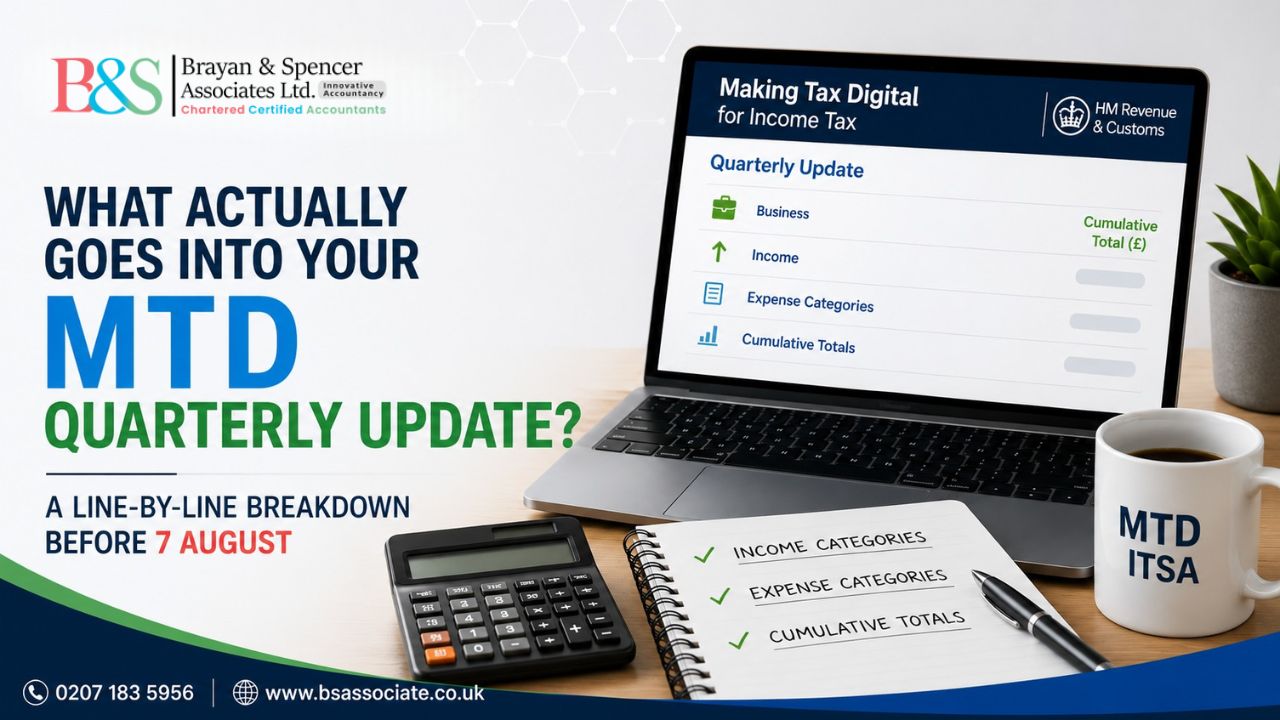

Your first quarter under Making Tax Digital for Income Tax closed on 5 July. The deadline to submit it is 7 August. So, here’s the question nobody’s answered yet: what actually goes in it?

If you’ve already read about the deadline itself, you know the date. What you probably don’t know is what to type into your software when you sit down to file it. Most guidance on MTD ITSA stops at “submit a summary of your income and expenses” and leaves it there. That sentence is technically true and completely useless at the moment you’re staring at a blank form.

Here’s what a quarterly update is built from, category by category, plus the one mechanic (cumulative totals) that catches almost everyone out by their second or third submission.

Quick answer: A quarterly update under MTD for Income Tax reports on income and expenses using HMRC’s fixed category list, split separately for each business you run. Self-employment and property are always reported as distinct businesses, even if it’s the same person filing both. Figures are cumulative from the start of the tax year, not just the three months just gone, and provisional figures are accepted as long as they’re corrected later.

The First Rule: Your Businesses Are Reported Separately

If you’re self-employed and you also let out a property, HMRC does not want one combined update. You file a quarterly update for your self-employment business and a separate one for your property business, even though both are due on the same date.

This matters for Digital Tax Reporting UK compliance because it changes how your software needs to be set up. A single spreadsheet with everything lumped together won’t map cleanly onto HMRC’s submission format. Your accounting software (or bridging software, if you’re using spreadsheets) needs to keep these as genuinely separate ledgers from day one, not something you split apart at filing time.

One exception worth knowing: if you own more than one UK rental property, HMRC treats all of them together as a single UK property business. A holiday taxed under the Furnished Holiday Lettings rules, and any overseas property, are each treated as their own separate business again.

What Counts as Income in a Quarterly Update

For a self-employment business, income means:

- Turnover from sales of goods or services

- Any other business income, for example insurance proceeds relating to the business

For a property business, income means:

- Rent received

- Other property income, such as insurance payouts related to the property or income from services provided to tenants, like a cleaning charge bundled into the rent

What doesn’t belong in a quarterly update at all: dividends, savings interest, pension income, PAYE employment income, and capital gains. These sit outside MTD entirely and only appear later, at your Final Declaration. If you’re used to your accountant handling everything as one bundle at year-end, this is the biggest mental shift. HMRC Quarterly Updates are narrower than a full tax return by design, and they’re meant to stay that way.

What Counts as an Expense: HMRC’s Actual Categories

This is where most confusion sits, because HMRC doesn’t want a single “expenses” total. Compatible software requires you to allocate spend into set categories. For a self-employment business, the standard categories include:

- Cost of goods bought for resale or used in providing services

- Car, van and travel expenses

- Wages, salaries and staff costs

- Rent, rates, power and insurance costs for premises

- Repairs and maintenance

- Phone, fax, stationery and other office costs

- Advertising and business entertainment costs

- Interest and bank/credit card financial charges

- Irrecoverable debts written off

- Professional fees (accountancy, legal, and similar)

- Other allowable business expenses

- Depreciation and loss/profit on sale of assets, reported but not tax-deductible, so your software should flag these as disallowable

For a property business, the categories shift to reflect letting activity: rent, rates, insurance and premiums; property repairs and maintenance; loan interest and other financial costs; legal, management and other professional fees; costs of services provided, including wages; and other allowable property expenses.

The practical implication for HMRC MTD Compliance: your digital records need to be tagged into these categories as you go, not reconstructed from a shoebox of receipts the week before filing. If your current software just tracks “money in, money out,” it isn’t doing enough to support an accurate quarterly submission under MTD for Income Tax.

The Mechanic Nobody Explains Well: Cumulative Totals

Here’s the part that catches out almost every first-year filer. A quarterly update is not a report of that quarter in isolation. It’s a running cumulative total from 6 April to the end of that period.

So, your Q1 update (6 April to 5 July) reports Q1 figures alone, because it’s the first one. Your Q2 update (6 April to 5 October) doesn’t report just July, August and September on their own; it reports the whole six months from 6 April, restating Q1’s numbers with Q2 activity added on top. Q3 restates for the first nine months. Q4 restates the full year.

This has a real consequence for anyone planning to “get it roughly right in Q1 and tidy it up later.” Because each later submission carries the earlier figures forward, an estimate baked into Q1 doesn’t stay contained to Q1. It flows through every subsequent update until you actively correct it. That’s not a problem if you’re aware of it and go back to fix the estimate in Q2. It becomes a genuine mess if three quarters go by before anyone notices the June invoice that was guessed at was £2,000 out.

The upside of cumulative reporting is that it’s genuinely self-correcting. Get a number wrong in Q1? You don’t need to resubmit Q1. You simply correct the running total in your next update, and the year-to-date figure catches up.

Can You Use Estimated Figures for These Categories?

Yes, category by category. If a supplier invoice for June hasn’t landed by your 7 August deadline, you can put in a reasonable estimate for that expense line and correct it once the real figure comes in, either in your next quarterly update or at the Final Declaration. What you can’t do is skip a category entirely because you’re not sure or delay the whole submission waiting for one outstanding invoice. HMRC’s stated preference under Making Tax Digital for Income Tax is a filed estimate over a missed deadline.

A Worked Example

Take a self-employed graphic designer with a rental flat. For Q1 (6 April to 5 July), her self-employment update reports turnover of £14,200, professional fees of £600, phone and office costs of £310, and car/travel expenses of £480. Separately, her property update reports rent received of £3,600 and property repairs of £250.

Come Q2, she doesn’t start a fresh count. Her self-employment update for the six months to 5 October will show cumulative turnover (Q1’s £14,200 plus everything invoiced July to September), with each expense category similarly running forward from the same April start point. Two entirely separate submissions, two entirely separate cumulative timelines, both due on the same 7 November deadline.

Getting Your Categories Right Before 7 August

If you’re still mapping your bookkeeping to these categories with days to go before the deadline, the priority now is accuracy over completeness. A well-estimated category beats a guessed-at lump sum, and both beat a missed submission.

At Brayan & Spencer Associates, we set up your MTD-compatible software to map correctly to HMRC’s income and expense categories from day one, keep your self-employment and property businesses properly separated, and manage your Quarterly Tax Returns UK submissions so the cumulative totals stay accurate quarter after quarter. We also provide the accounting software itself at no extra cost, so there’s nothing extra to budget for. Call 0207 183 5956 or visit www.bsassociate.co.uk to get your categories right before your next filing.

Frequently Asked Questions

No. HMRC requires them as separate quarterly updates, even though both are due on the same date under MTD ITSA.

Cumulative. Each update restates the whole tax year to date, not just the latest quarter.

Yes. Provisional figures are accepted by category and can be corrected in a later update or at the Final Declaration.

Dividends, savings interest, pension income, PAYE employment income, and capital gains. These are only reported at the Final Declaration, not through HMRC Quarterly Updates during the year.