Every piece of Making Tax Digital coverage right now is aimed at one group: sole traders and landlords with qualifying income over £50,000, who just filed their first quarterly update by 7 August 2026. That’s the right story for this month. But it’s created a blind spot for a much larger group who will be mandated into Making Tax Digital for Income Tax from April 2027, and who currently have almost nothing written for them.

Quick answer: If your combined gross income from self-employment and property was between £30,000 and £50,000 in the 2025/26 tax year, you’ll be brought into MTD for Income Tax from 6 April 2027, the second phase of the rollout. Your qualifying income is assessed from your 2025/26 Self Assessment return, the one due by 31 January 2027, which means the return you’re about to file is the one that decides whether you’re mandated next April. The reporting structure is identical to Phase 1: four quarterly updates (due 7 August, 7 November, 7 February, 7 May) plus a Final Declaration. What’s different is that Phase 2 taxpayers do not get the same soft landing Phase 1 received, so there’s less room to learn on the job.

Why This Matters Now, Not in Twelve Months

It’s tempting to treat April 2027 as distant. It isn’t, for one specific reason: the tax return that determines your Phase 2 status is the one covering 2025/26, due by 31 January 2027. That’s roughly six months away. Whatever gross income figure lands on that return effectively decides whether you’re mandated into quarterly digital reporting a few months later.

That timing creates a narrow but real planning window right now. If your turnover is hovering near £30,000, whether you’re just under or just over changes your obligations for years, since once you’re brought into MTD, dropping back under the threshold in a later year doesn’t automatically take you back out. HMRC only releases taxpayers who fall below the threshold for three consecutive years. A single strong year, or a single year where you under-record income and later must restate it, can lock in obligations that follow you well beyond 2027/28.

Who Actually Falls Into This Group

Phase 2 catches a wider and more varied group than Phase 1 did. Consider a self-employed physiotherapist in Hackney who also rents a single buy-to-let in Croydon. Individually, neither income stream looks large. Combined gross turnover, before any expenses, mortgage interest, or allowances, is what counts, and for many people running a modest sole trade alongside one rental property, £30,000 to £50,000 combined is an entirely ordinary position, not an especially high-earning one.

This is the detail that consistently surprises people in this income band: qualifying income is turnover, not profit. A landlord with £34,000 in gross rent and £9,000 in mortgage interest and letting agent fees is still assessed on the £34,000 figure, not the £25,000 left over after costs. Someone who has never thought of themselves as needing “proper” accounting software can still be squarely inside Phase 2 without realising it.

The Lesson Phase 1 Already Taught Us

Watching how the £50,000 cohort’s first quarterly update went in August 2026 gives Phase 2 taxpayers a genuine advantage, if they take it. The pattern that emerged wasn’t complicated: people who signed up for MTD and connected their software months in advance had a routine first submission. People who left sign-up, software selection, and digital record-keeping until June and July spent the final weeks before the deadline retrofitting three months of transactions into a system they’d never used, while trying to get HMRC authorisation working under time pressure.

Phase 2 does not carry the same soft landing that protected Phase 1’s first submissions from penalty points. That protection was explicitly for the first cohort brought in from April 2026, and current guidance does not extend it to the 2027 wave. That changes the stakes of a late or scrambled first submission considerably. A missed quarterly deadline in Phase 2’s first year is a penalty point from day one, not a consequence-free learning exercise.

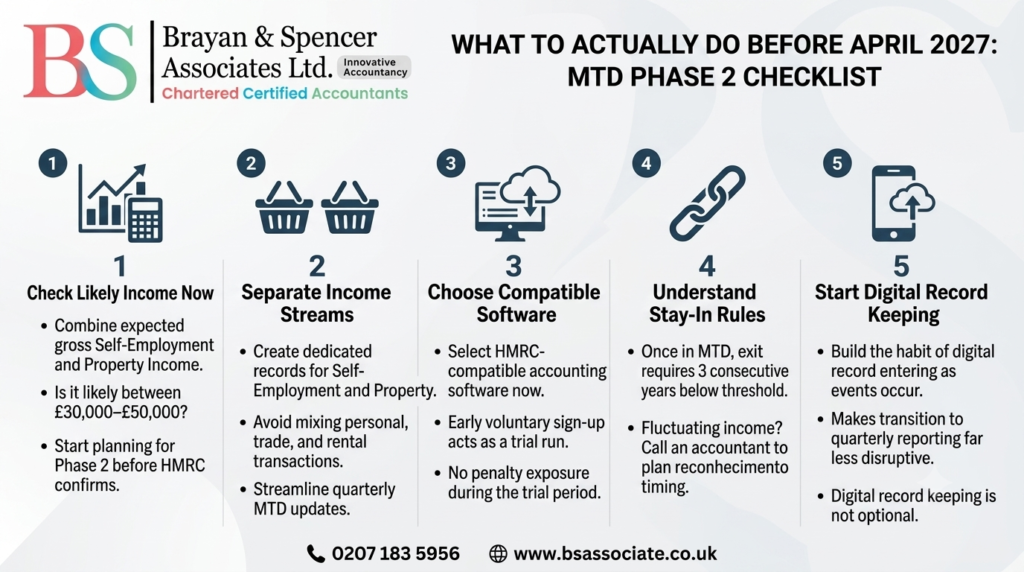

What to Actually Do Before April 2027

1. Check your likely qualifying income now, not after your 2025/26 return is filed.

Add your expected gross self-employment turnover to your gross rental income for the current tax year. If the combined figure looks likely to land between £30,000 and £50,000, start planning as though Phase 2 applies to you, rather than waiting for HMRC to confirm it after the fact.

2. Separate your income streams in your records now.

Self-employment and property income need their own quarterly updates once you’re in MTD. Bank accounts and spreadsheets that mix personal, trade, and rental transactions together create far more work later than keeping them apart from the start.

3. Choose HMRC-compatible accounting software before you’re mandated, not after.

You don’t need to wait for April 2027 to start using MTD-compatible software. Many sole traders and landlords in the £30,000 to £50,000 band voluntarily sign up early, using the year before mandation as a trial run with no penalty exposure, since the requirement to file simply doesn’t apply yet.

4. Understand that once you’re in, you generally stay in.

Because exit from MTD requires three consecutive years below the threshold, a single high-turnover year doesn’t just affect that year’s obligations. Speak to an accountant if your income fluctuates near the £30,000 line, since the timing of when income is recognised can matter more than it would under the old annual Self Assessment system.

5. Don’t assume digital tax reporting UK rules mean digital record keeping is optional in the meantime.

Even before mandation, building the habit of entering income and expenses digitally as they occur, rather than reconstructing them from memory in January, makes the transition to quarterly HMRC reporting far less disruptive whenever your mandation date arrives.

A Note on Timing and Threshold Changes

The rollout of Making Tax Digital for Income Tax has already shifted more than once, and the £20,000 threshold planned for April 2028 remains the next confirmed stage after Phase 2. None of that changes the practical point for anyone currently between £30,000 and £50,000: the return you file for 2025/26 is the one that matters, and preparing your records and software choice in the months before that filing gives you a materially easier first quarterly update than treating April 2027 as a start date to think about later.

For background on how the first phase of MTD for Income Tax has worked in practice, read our guide on Making Tax Digital for Income Tax for UK sole traders and landlords, and for the full run of HMRC quarterly deadlines through the current tax year, see our MTD for Income Tax quarterly deadline guide. Our full archive of MTD coverage, including the mistakes made during the first quarterly cycle, is available on our Making Tax Digital blog category page.

Get Ahead of Phase 2 Before HMRC Confirms Your Status

If your combined income sits anywhere near the £30,000 threshold, the return you’re preparing for 2025/26 deserves a proper review now, not a rushed filing in January 2027 followed by a scramble to get MTD-compliant software running by April. At BS Associate, we help sole traders and landlords across London assess their likely Phase 2 status, choose the right HMRC-compatible accounting software, and build clean digital records well before mandation, rather than after.

Visit www.bsassociate.co.uk or call 0207 183 5956 to get your Phase 2 readiness assessed.

Frequently Asked Questions

From 6 April 2027, based on qualifying income reported on the 2025/26 Self Assessment return, which is due by 31 January 2027.

Turnover. Qualifying income is gross income from self-employment and property combined. Before expenses, mortgage interest, or allowances are deducted.

Current guidance limits the penalty-free soft landing to the first cohort mandated from April 2026. It has not been confirmed for the 2027 intake, so late quarterly updates in Phase 2’s first year carry a real risk of penalty points from the outset.

Yes. Voluntary early sign-up is available and lets you test HMRC-compatible accounting software and quarterly reporting without a filing obligation attached yet.

Only after your qualifying income has fallen below the relevant threshold for three consecutive tax years. A single lower-income year does not remove you from MTD.

No, but you do need to keep the two income sources separate within your digital records, since each requires its own quarterly update once you’re in MTD for Income Tax.

Estimate your 2025/26 combined gross income before you file that return in January 2027, and if it’s likely to fall between £30,000 and £50,000, start separating your records and researching HMRC-compatible software immediately rather than waiting for confirmation of your mandation date.