If you jointly own a rental property, you may already be splitting the income and declaring it each year. On the surface, it seems straightforward.

However, with the introduction of Making Tax Digital, the way rental income is recorded and reported has changed in a way that many landlords are still adjusting to.

Under Making Tax Digital for Income Tax Self Assessment (MTD for ITSA), you are no longer submitting one combined annual figure. Instead, each owner must:

- Keep their own digital records

- Report their share of income separately

- Submit updates to HM Revenue and Customs throughout the year

This means HMRC now receives multiple submissions linked to the same property, making it easier to identify inconsistencies between joint owners.

In practice, this is where many issues arise and small mistakes can quickly lead to compliance problems if not handled correctly.

Quick Answer

- Each owner reports their own share of rental income, not the total

- Income must follow beneficial ownership

- Expenses must be split in the same ratio as income

- Each owner submits separate quarterly updates

- Inconsistent reporting can trigger HMRC checks

The Core Rule: Tax Follows Ownership, Not Convenience

The most important principle is simple:

You are taxed on your share of the property, not on who receives the rent or manages the property.

This applies across:

- Making Tax Digital for landlords

- Making Tax Digital for Income Tax Self Assessment

If this rule is misunderstood, it is one of the main reasons joint landlords face reporting issues.

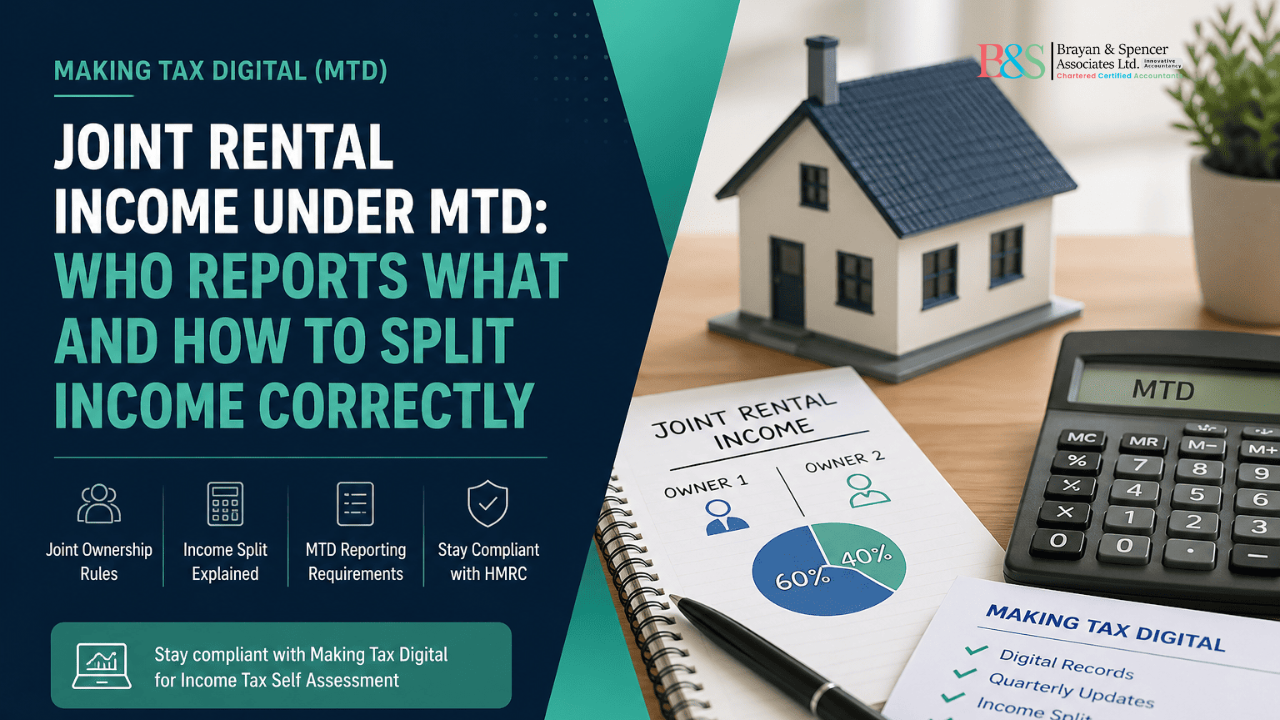

How Rental Income Should Be Split

Married Couples or Civil Partners

- Default split is 50:50

- To declare a different split, you must submit Form 17

- Supporting evidence is required

Other Joint Owners

Income is split based on:

- Ownership percentage

- Legal agreements

- Financial contribution

Each owner must report only their share.

Real Scenarios Where Landlords Get It Wrong

Scenario 1: One Person Receives All the Rent

Even if rent is paid into one account, each owner must still report their share.

Scenario 2: Ownership and Income Do Not Match

If ownership is 60:40, income must follow that split unless formally declared otherwise.

Scenario 3: Expenses Claimed by One Owner

Expenses must be divided in the same ratio as income, not claimed by one person alone.

Scenario 4: Different Figures Submitted

If joint owners submit different figures, HM Revenue and Customs may identify inconsistencies.

What Has Changed Under Making Tax Digital

Before MTD:

- One annual return

- Limited visibility of discrepancies

Under MTD:

- Quarterly reporting

- Digital records

- Greater transparency for HMRC

This makes accurate and consistent reporting far more important.

Step by Step: How to Stay Compliant

To meet Making Tax Digital for Income Tax Self Assessment requirements:

- Confirm your ownership split

- Record income based on that split

- Allocate expenses in the same ratio

- Keep separate digital records

- Use reliable Making Tax Digital software

- Ensure both owners submit consistent figures

Practical Example

Property ownership:

- Owner A: 60%

- Owner B: 40%

Monthly rent: £1,000

Reporting:

- Owner A: £600

- Owner B: £400

Expenses (£200):

- Owner A: £120

- Owner B: £80

Each owner submits their figures separately.

Where HMRC Is Most Likely to Challenge

According to HM Revenue and Customs, issues are more likely where:

- One owner reports all income

- Ownership percentages are inconsistent

- Expenses do not match income ratios

- Joint owners submit different figures

These checks are based on data consistency rather than random selection.

Why Proper Structuring Matters

Joint rental income becomes more complex when:

- Ownership is unequal

- Contributions differ

- One person manages finances

In these cases, applying HMRC rules correctly requires a structured approach.

At Brayan & Spencer Associates, the focus is on helping landlords:

- Align ownership with reporting

- Maintain accurate digital records

- Ensure consistency across submissions

This reduces the risk of errors under Making Tax Digital.

Need Help Understanding Your MTD Reporting?

If you are unsure how your joint rental income should be split or reported under Making Tax Digital for Income Tax Self Assessment, it is worth reviewing your position before your next submission.

📞 Call us at 0207 183 5956 or visit www.bsassociate.co.uk

Conclusion: Getting Joint Rental Income Right Under MTD

Joint rental income has always required careful handling, but under Making Tax Digital, the margin for error is much smaller.

The key challenge is no longer just understanding the rules — it is applying them consistently across separate digital submissions. Because each owner now reports individually, even small differences in income, expenses, or ownership percentages can create inconsistencies that are visible to HM Revenue and Customs.

In practical terms, most issues arise when:

- Income is reported by one owner instead of being split

- Ownership and income percentages do not match

- Expenses are not allocated correctly

- Records between owners are not aligned

A clear and consistent approach is essential:

- Confirm how the property is owned

- Apply that split consistently

- Keep accurate digital records

- Ensure all submissions match

As Making Tax Digital for Income Tax Self Assessment continues to reshape reporting, landlords who structure their records properly from the outset are far better placed to remain compliant and avoid unnecessary complications.

Frequently Asked Questions:

Ans: Each owner must report only their share of the rental income, even if the full rent is paid into one bank account. Under Making Tax Digital, tax is based on ownership, not who collects the money.

Ans: No, unless it is formally declared. For married couples, a different split must be reported using Form 17 with supporting evidence. Without this, income must follow ownership proportions.

Ans: Yes. Under Making Tax Digital for Income Tax Self Assessment, each owner must:

Keep their own digital records

Submit quarterly updates

Report their individual share

There is no option for a combined submission.

Ans: If figures do not match, HM Revenue and Customs may flag the difference. This can lead to:

Data inconsistencies

Requests for clarification

Possible compliance checks

Both owners should ensure their figures align before submission.

Ans: Expenses must be divided in the same ratio as income. For example, if ownership is 70:30, both income and expenses must follow that split, regardless of who paid the costs.

Ans: The key rule is:

Each owner must report their own share of rental income and expenses accurately, with consistent figures across all submissions.

This is the foundation of compliance under Making Tax Digital for landlords.