Picture a self-employed electrician named Daniel who also rents a one-bed flat in Leeds. His combined turnover from the two pushed him just over £50,000 last year, so from 6 April 2026 he became one of the first people in the country required to file under Making Tax Digital for Income Tax. Walking through what happens to someone like Daniel, quarter by quarter, makes the new system far less abstract than reading another list of dates and rules.

Day One: 6 April Came and Went, Now What?

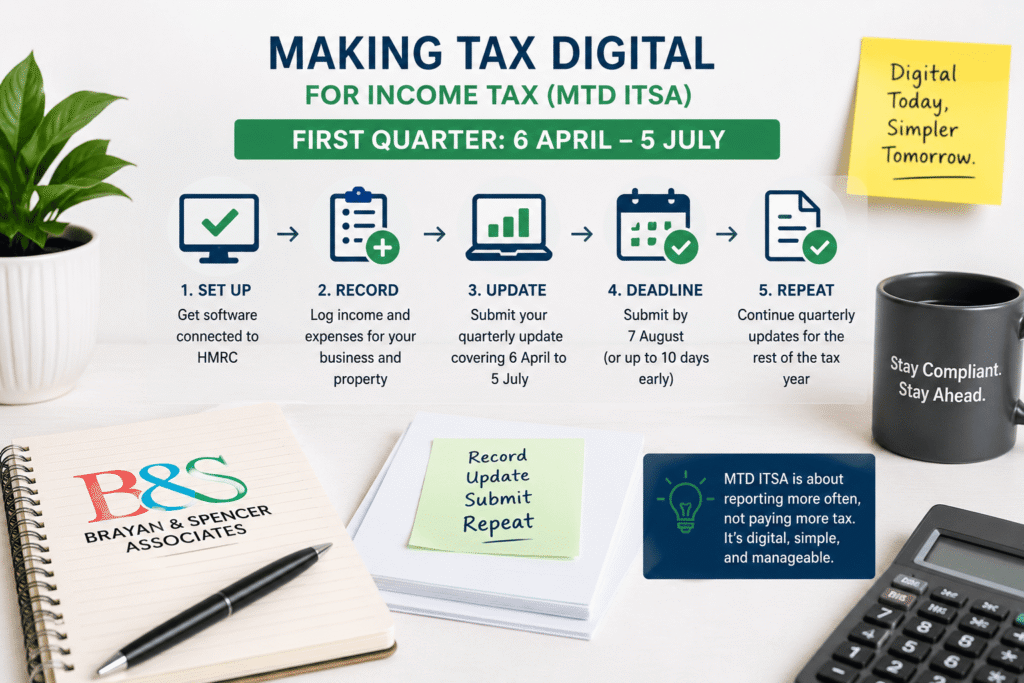

Nothing changed on the day itself. Daniel didn’t open an app or fill in a form on 6 April. What changed is that every transaction from that date onward now belongs to a reporting period that ends on 5 July, with a submission due to HMRC by 7 August. For Daniel, that meant his usual habit of dealing with paperwork “whenever he got round to it” stopped being workable. MTD ITSA runs a quarterly clock, and the clock had already started.

Where the £50,000 Threshold Catches People Out

Daniel almost missed that he was in scope at all, because he was thinking about profit, not turnover. His electrical work brought in roughly £38,000 before expenses, and his flat brought in £14,000 in rent. Individually, neither figure looks like much. Added together as gross income before any costs are deducted, they came to £52,000, which is what actually determines mandation under MTD for Income Tax. This is one of the most common reasons people assume they’re exempt when they’re not: the threshold is based on combined gross income from self-employment and property, not net profit.

Getting Software Connected Before the Numbers Even Matter

The part of the process that took Daniel the most time wasn’t his bookkeeping; it was getting software linked to HMRC in the first place. He couldn’t use HMRC’s standard online account for this; anyone within MTD for Income Tax needs either dedicated accounting software or a spreadsheet paired with bridging software that can submit data digitally. Either route needs to be set up and connected to HMRC before a quarterly update can be sent, which makes leaving this until late July a genuinely risky move.

This is also the stage were having an accountant who already handles HMRC MTD compliance for other clients makes a tangible difference. At Brayan & Spencer Associates, we provide free accounting software as part of our service, connect it to HMRC on the client’s behalf, and configure it for whatever mix of income sources they have so nobody is left figuring out bridging software alone two weeks before a deadline.

What Daniel’s First Quarterly Update Actually Contains

Once the software was connected, Daniel’s job was record-keeping, not arithmetic. His electrical income and expenses (van costs, materials, tools) went in as one figure set; his rental income and expenses (letting agent fees, a repair bill, landlord insurance) went in as a separate set, because self-employment and property are reported as distinct income sources even though they’re combined for the threshold test. Neither figure needed to be a finished tax calculation; these HMRC quarterly updates are summaries of totals, not a Self-Assessment in miniature, and no tax is worked out or paid at this stage.

This is worth repeating because it’s where a lot of confusion sits: people search for “quarterly tax returns UK” expecting something resembling an annual return done four times a year. It isn’t. There’s no liability calculated, no payment triggered, and no final figure confirmed that all happens later, at the Final Declaration.

Pressing Submit: What Actually Happens

For Daniel, submitting meant his software sent HMRC a year-to-date total covering 6 April to 5 July, built from the categorised figures he’d entered. Because updates are cumulative, this isn’t a one-off snapshot; his next submission in November will include this quarter numbers plus the next one, with any corrections folded in automatically rather than filed separately. He could have submitted up to ten days before 5 July if his records were already complete; there’s no requirement to wait until the deadline itself.

The Soft Landing Isn’t a Free Pass

One thing Daniel almost got wrong: if because 2026/27 carries no penalty points for late quarterly updates, the 7 August date doesn’t really matter this year. It does. HMRC won’t issue a points-based fine for a late first update during this soft-landing year, but it still must be filed with all four quarterly updates for the year need to be in before HMRC will accept the Final Declaration that follows. Treating the first deadline as optional just shifts the workload later, when three other updates will be competing for attention as well. From 2027/28, missed deadlines start accumulating penalty points, with a £200 fine once four points build up.

Building a Habit Daniel Wishes He’d Started Sooner

By the time his first submission went in, Daniel admitted the hardest part wasn’t the software or the threshold it was breaking a year-long habit of letting receipts pile up in a glovebox until tax season. MTD doesn’t really care how you keep records day to day, as long as the end result is digital, accurate, and categorised correctly. What it does remove is the option of doing that work once a year.

For his second quarter, running from 6 July to 5 October, Daniel set aside fifteen minutes most Friday afternoons to log invoices and receipts rather than waiting for a quiet month. It’s a small change, but it’s the difference between a quarterly update taking an afternoon and one taking a weekend. Anyone newly in scope for Making Tax Digital for Income Tax is better off building that rhythm now, in this first quarter, rather than discovering how unmanageable a backlog becomes three updates from now.

If Your First Quarter Looks Like Daniel’s

Most people brought into MTD this year are juggling exactly this kind of mixed picture a main trade or job alongside a rental property, or a side business that’s grown past the point of casual record-keeping. Getting the first quarterly update right mostly comes down to sorting the groundwork early: confirming you’re genuinely in scope, getting software connected to HMRC well before the deadline, and keeping income and expenses properly categorised as you go rather than reconstructing three months of records in late July.

At Brayan & Spencer Associates, this is the kind of digital tax reporting UK businesses ask us to take off their hands entirely. We provide free accounting software, link it to HMRC, and manage the quarterly submissions ourselves, so clients like Daniel don’t have to think about the mechanics at all. Call us on 0207 183 5956 or visit www.bsassociate.co.uk before 7 August if you’d like us to handle yours.

Quick-Fire Questions from Clients Like Daniel

No that only happens at the Final Declaration stage, after the tax year ends.

You can correct it. Because each update is cumulative, an error caught in a later quarter or year-end automatically adjusts what was reported earlier.

No. All UK property income is combined into one update stream, regardless of how many properties you hold; self-employment income from a separate business is reported on its own.

No. The 31 January and 31 July payment dates are unchanged quarterly updates only affect how often you report, not when you pay.